Two Months In

It is two months into 2026, and what do we have to show for it? From a US perspective, investors are moving away from vulnerable market segments, particularly those disrupted by artificial intelligence (AI).

Business lines that once relied on outsourcing are increasingly being replaced by what is called an “AI leveraged service model” or “digitally augmented resourcing.”

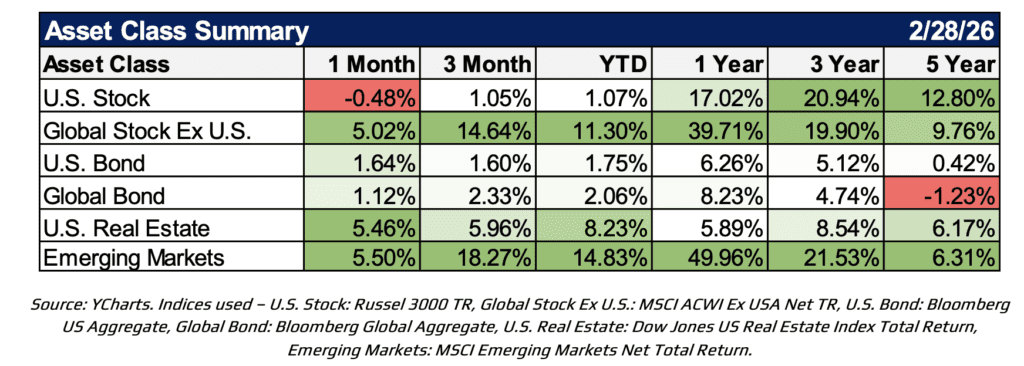

At the same time, market leadership is broadening globally as emerging markets lead, small caps gain, and large-cap growth stocks pare losses amid capital rotation toward value-oriented areas.

The so-called “Magnificent Seven” stocks lagged in February, falling 7.3%, largely due to rising concerns around capital expenditures. Investors have grown increasingly cautious about the massive AI-related spending plans announced by companies such as Amazon, Alphabet, and Meta Platforms. Each of these firms signaled sharply higher investment in AI infrastructure, which could weigh on near-term profitability.

Rotation²

This brings us to a rotation within the rotation. Companies directly tied to the AI ecosystem, from semiconductor manufacturers to those who deploy the technology, have benefited in recent years.

Even as companies continue to report strong earnings, the market has begun to question whether the long-term earnings assumptions embedded in some valuations may be overly optimistic or just not worth owning, given the trade-off between upside and potential losses and how markets react to the slightest disruptive news.

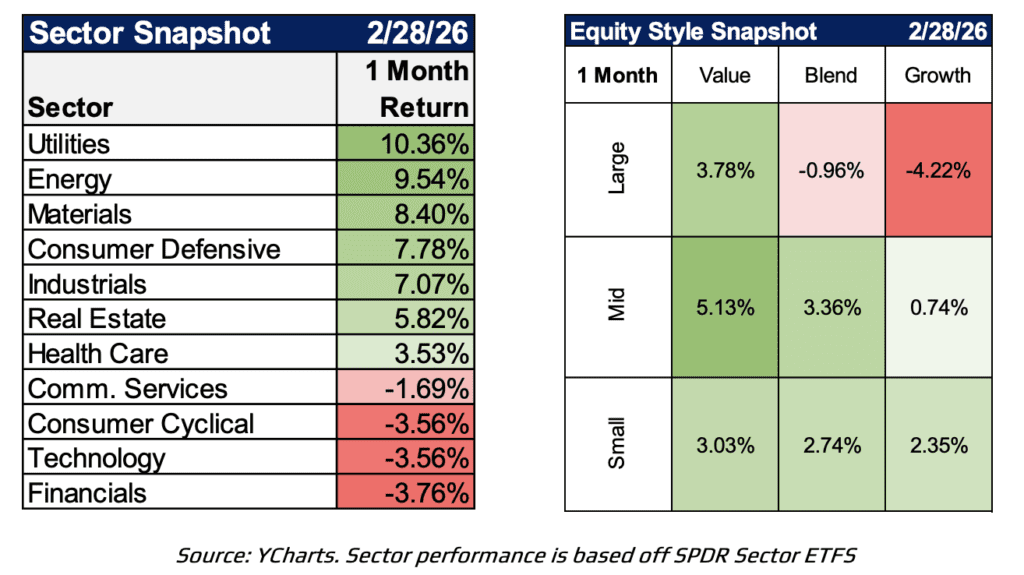

At the same time, the enormous energy requirements of AI infrastructure are increasingly attracting attention, especially in recent months. Over the past month, we have seen a noticeable resurgence, no pun intended, in utility stocks. In an environment where investors are increasingly uncertain about where the next technological disruption might occur, some capital has rotated toward areas tied to a more fundamental and unavoidable need: power. Data centers and AI infrastructure require enormous amounts of electricity, along with the cooling systems needed to manage that demand.

The energy sector has also benefited from this environment. Many have emphasized dividends and share repurchases supported by strong free cash flows. Rising oil prices, fueled in part by geopolitical tensions between the United States and Iran, have provided an additional tailwind for the sector. Meanwhile, some of the former growth leaders that drove market performance in recent years have repriced meaningfully lower.

Suffice it to say, the seemingly defensive move within the AI space seems to be exposure to, either directly or indirectly (cooling systems), to the need for power. Oil and natural gas are a different story, though.

Looking Beneath the Surface of Job Growth

Looking deeper into recent economic data, the job growth picture is more complex than the headlines suggest.

Headline employment numbers remain positive, but most net job gains come from healthcare and private education, while many other sectors are shedding jobs.

What does this mean? It could suggest that the widely discussed broadening of economic growth may be narrower than previously expected, which could eventually show up in future earnings across affected sectors. On the other hand, it could also indicate that productivity gains from AI are allowing companies to maintain or expand profit margins while reducing workforces that expanded significantly during the pandemic. Reality may very well be a combination of both.

Geopolitics and Energy Markets

It would also be difficult to discuss the current market environment without addressing rising geopolitical tensions involving Iran even though the events are captured in February’s global performance.

The primary concern in the US is that higher global fuel prices could potentially reignite inflation. However, because the US is now a net energy exporter, the overall impact on domestic economic growth may be somewhat limited, likely showing up primarily as moderately higher pump prices.

The Strait of Hormuz accounts for only a small share of US energy imports, so reduced activity there is not seen as a major domestic issue. However, prolonged conflict could affect global energy markets and economies that depend more on the region. We are monitoring this closely to manage potential risks.

Private Markets Come Back into Focus

Private credit has returned to the spotlight. With the Tricolor default behind us, recent loan sales by Blue Owl Capital have renewed attention on these markets. Despite increased scrutiny, many loans cleared near par value, indicating valuations remain relatively stable as investors watch conditions.

More broadly, private credit is undergoing a stress test as valuations for technology and software companies, particularly in the SaaS space, are resetting lower. Many credit vehicles were built on assumptions of consistently rising recurring revenue multiples. As those multiples normalize, lenders are reassessing credit risk while the SaaS market itself is being repriced toward more sustainable valuation levels.

What we are beginning to see is a clearer separation between high-quality companies with durable growth and profitability and weaker players that previously benefited from abundant capital. That distinction is increasingly influencing both capital allocation and credit underwriting across private markets.

Tax Season: An Opportunity for Planning

As we move further into the year, it is also worth remembering that tax season is approaching. This is an important time to connect with your advisor and review your broader financial plan.

Investors should be mindful of potential capital gains distributions from mutual funds, as well as taxable income from dividends and interest payments. For those holding exchange-traded funds or actively managed funds in taxable accounts, understanding where income may be generated can help avoid surprises when filing taxes.

This is also a good opportunity to review carry-forward losses from prior years, which may help offset realized gains, and to evaluate tax location strategies to ensure income-generating assets are placed in the most tax-efficient accounts possible. Thoughtful planning around these factors can make a meaningful difference in after-tax returns over time.

Staying Focused on the Long Term

Markets will always go through periods of adjustment as technology evolves, capital flows shift, and new risks emerge. While headlines can sometimes make these transitions feel more dramatic than they truly are, it is important to remember that markets had historically navigated periods of uncertainty before.

Our focus remains on maintaining diversified portfolios, managing risk thoughtfully, and positioning investments to participate in long-term growth opportunities.

As always, if you have questions about the current environment or how these developments may affect your portfolio, please do not hesitate to reach out. We appreciate the trust you place in us and look forward to continuing to navigate the year ahead together.

From the Investments Desk at Journey Strategic Wealth

This material is distributed for informational purposes only. Investment Advisory services offered through Journey Strategic Wealth, an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). The views expressed are for informational purposes only and do not take into account any individual’s personal, financial, or tax considerations. Opinions expressed are subject to change without notice and are not intended as investment advice. Past performance is no guarantee of future results. Please see Journey Strategic Wealth’s Form ADV Part 2A and Form CRS for additional information.